DD: Aurinia Pharmaceuticals ($AUPH)

Rating: BULLISH | Target Price: $24.64 | Current Price: $15.72 | Implied Upside: +56.7%

AUTHOR’S TAKE

I am bullish on Aurinia Pharmaceuticals because the market currently undervalues the durability of LUPKYNIS as it approaches standard-of-care status in lupus nephritis while simultaneously assigning near-zero value to the burgeoning aritinercept (AUR200) pipeline and the newly acquired zetomipzomib. Aurinia’s recent pivot from a commercial-stage company into a lean, development-heavy entity following the March 2026 appointment of Kevin Tang as CEO and the subsequent $300M+ acquisition of Kezar Life Sciences will unlock operating leverage. The most important near-term catalyst is the upcoming mid-2026 disclosure of Phase 2 PALIZADE data for zetomipzomib and trial initiations for aritinercept in a second autoimmune indication. I view the current cash position and the $305 million to $315 million net sales floor for 2026 as providing a fundamental floor of $10.00 to $11.00. Even applying a conservative 10-15% discount to account for clinical execution risk, the stock maintains a high-conviction support level near $9.00, representing significant downside protection relative to current trading prices.

STRATEGY AND PIPELINE

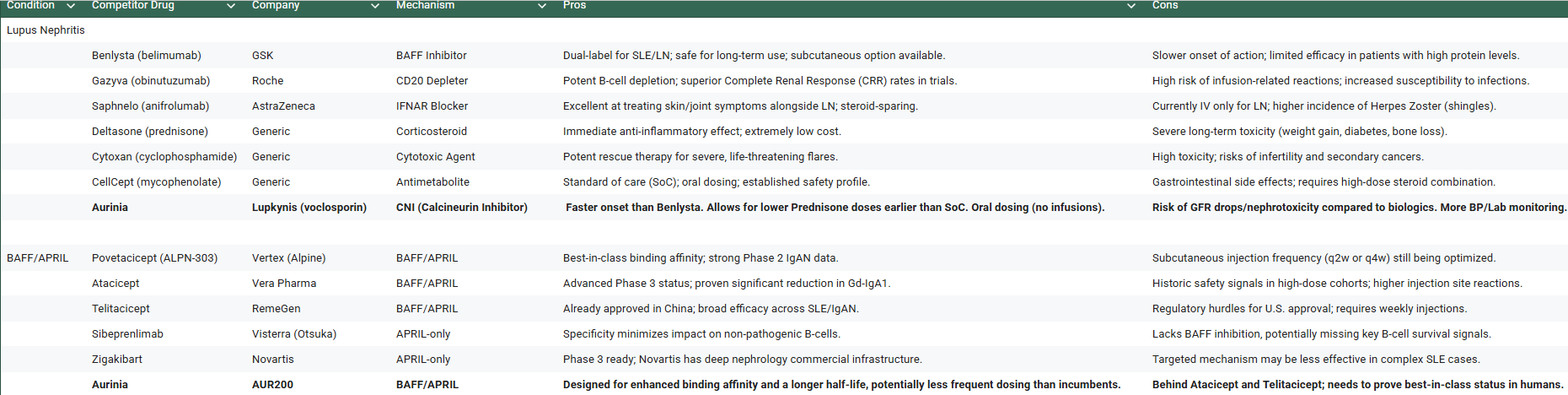

Aurinia’s primary value driver is LUPKYNIS, the first FDA-approved oral therapy for active lupus nephritis. LUPKYNIS is a calcineurin inhibitor with a dual mechanism of action: it stabilizes podocytes in the kidney to reduce proteinuria and inhibits T-cell activation to dampen the autoimmune response. The company generates revenue through direct product sales in the U.S. and royalty/collaboration revenue from Otsuka Pharmaceuticals in Europe and Japan. Strategically, Aurinia has evolved from a single-asset commercial story into a diversified immunology player by advancing aritinercept, a potent recombinant fusion protein that inhibits both BAFF and APRIL. This dual inhibition is critical because it targets a broader range of B-cell stages than current therapies like Benlysta. The pipeline’s importance lies in its ability to extend the company’s terminal value beyond the LUPKYNIS patent cliff in the late 2030s.

CLINICAL PERFORMANCE AND METHODOLOGY

The foundational clinical evidence for LUPKYNIS stems from the pivotal Phase 3 AURORA 1 study and its long-term extension, AURORA 2. In AURORA 1, patients treated with LUPKYNIS in combination with mycophenolate mofetil and low-dose steroids achieved a statistically significant Complete Renal Response rate of 40.8% at 52 weeks, compared to 22.5% in the control arm (p < 0.001). Key efficacy data showed a faster and more significant reduction in the protein-to-creatinine ratio without the traditional CNI-related side effects like glucose intolerance or significant electrolyte imbalances. The trial design was rigorous, utilizing a rapid steroid taper which demonstrated that LUPKYNIS can achieve efficacy while reducing steroid-induced morbidity. For aritinercept, Phase 1 data showed 100% BAFF/APRIL suppression at higher dose cohorts with a clean safety profile, setting the stage for the currently enrolling Phase 2 studies.

MOAT, IP, REGULATION, AND STRUCTURAL ADVANTAGES

Aurinia maintains a robust moat through a combination of regulatory exclusivity and a dense patent thicket. LUPKYNIS is protected by U.S. Patent No. 10,286,036, which covers the dosing protocol and extends protection until 2037. This method of use patent is a high barrier to entry for generics. Furthermore, LUPKYNIS enjoys New Chemical Entity exclusivity. In the LN market, Aurinia benefits from high switching costs; once a patient achieves renal stability, physicians are loath to alter therapy given the high risk of permanent kidney damage. The company’s specialized sales force and established relationships with nephrologists and rheumatologists create a commercial flywheel that is difficult for new entrants to disrupt.

THE BULL CASE

The bull case centers on LUPKYNIS exceeding the high end of 2026 guidance through increased penetration into the 100,000-patient U.S. LN market. Catalysts include positive Phase 2 proof-of-concept data for aritinercept in late 2026, which would re-rate Aurinia as a multi-asset immunology leader. The market is mispricing the stock by applying a low-growth terminal value, ignoring the potential for LUPKYNIS to reach $500M+ in peak sales and the optionality of a buyout. Under this scenario, a high peak revenue multiple plus pipeline NPV justifies a share price range of $22.00 to $26.00.

THE BEAR CASE

The bear case is defined by a potential plateau in LUPKYNIS adoption as competitive B-cell depleting therapies gain traction in earlier lines of treatment. Failure modes include a breakdown in the partnership with Otsuka or a safety signal emerging from the long-term use of aritinercept. If LUPKYNIS growth stalls below $350M and the pipeline fails to produce a viable second indication, the stock would likely trade down to its cash value plus a conservative multiple on declining sales. This results in a downside valuation range of $8.00 to $10.00 per share.

FINANCIAL POSITION, UNIT ECONOMICS, AND RUNWAY

As of early 2026, Aurinia reports $480.2 million in total current assets, including $378.8 million in cash and short-term investments. The company turned GAAP profitable in 2025 and reported a Q1 2026 net income of $34.4 million, a 48% year-over-year increase. Gross margins are exceptional at 92%, reflecting the low cost of manufacturing for an oral small molecule. With operating cash flows of $32.6 million in Q1, Aurinia is fully self-funded. This removes near-term dilution risk and allows the company to aggressively repurchase shares or pursue acquisitions.

ACQUISITION OF KEZAR LIFE SCIENCES

In May 2026, Aurinia strategically transformed its pipeline by completing the acquisition of Kezar Life Sciences for $6.955 per share in cash plus a Contingent Value Right (CVR). This acquisition secures zetomipzomib, a first-in-class selective immunoproteasome inhibitor that provides a clinical moat around the LUPKYNIS franchise. While LUPKYNIS remains the oral standard for induction therapy, zetomipzomib offers a distinct, non-immunosuppressive mechanism that could dominate the maintenance market or provide a critical alternative for refractory patients. Furthermore, the acquisition diversifies Aurinia into high-value orphan indications like Autoimmune Hepatitis (AIH), where the lack of FDA-approved therapies offers a path to Breakthrough Therapy Designation. By integrating Kezar’s assets, Aurinia has evolved from a single-product commercial company into a diversified immunology leader, significantly de-risking the long-term revenue profile as the market awaits mid-2026 PALIZADE data.

MARKET & COMPETITION

KEY CATALYSTS AND TIMELINE

Mid-2026: Initiation of Phase 2 clinical study for aritinercept in a second autoimmune indication.

Q3 2026: FDA negotiation update regarding pediatric post-marketing requirements for LUPKYNIS.

November 2026: Q3 2026 Earnings Report and potential upward revision of full-year guidance.

Late 2026: Preliminary Phase 2 data readout for aritinercept in the first autoimmune indication.

rNPV VALUATION

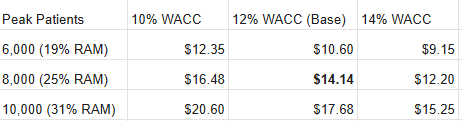

The target price of $24.64 is derived from a meticulous sum-of-the-parts risk-adjusted Net Present Value (rNPV) analysis that calculates the present value of all future cash flows through the 2037 patent expiry. For the primary LUPKYNIS U.S. commercial segment, I modeled a Total Addressable Market of 100,000 patients, filtered down to a Realistic Addressable Market of 32,000 biopsy-proven active LN patients currently under care. I applied a 25% peak market penetration (8,000 patients) by 2031 at a Gross WAC price of $90,000 per year, adjusted by a 15% Gross-to-Net (GTN) discount to reflect specialty pharmacy historicals and Q1 2026 margin stability of 92%. This results in $612 million in peak net sales. This segment uses a 100% Probability of Success (PoS) as an approved drug and a 12% WACC discount rate, accounting for a 30% SG&A and 5% maintenance R&D cost structure, resulting in an rNPV of $1.85 billion.

The AUR200 pipeline contribution of $485 million is derived by modeling it as a second-to-market dual BAFF/APRIL inhibitor with peak net sales of $435 million, assuming a 15% penetration in a primary autoimmune indication with 50,000 treated patients. The net price per patient is modeled at $75,000, derived from a $95,000 Gross WAC minus a 21% GTN discount to account for the more competitive broader autoimmune landscape. Given its clinical stage, I applied a standard 20% PoS for Phase 2 entry and a 15% discount rate to account for clinical execution risk. Following the May 2026 acquisition of Kezar, I have added zetomipzomib to the model with an rNPV of $320 million. This is based on a conservative 25% PoS (reflecting successful Phase 2a PORTOLA data) and a peak sales potential of $500 million across LN and Autoimmune Hepatitis (AIH), where “orphan” status supports a higher net price of $110,000. International royalties from the Otsuka partnership are valued at an rNPV of $240 million based on a 15% royalty on peak sales. Summing these parts with the $327.4 million cash balance—adjusted for the $51.4 million Kezar cash outlay—and dividing by 130.8 million fully diluted shares (reflecting the cumulative 23.1 million shares repurchased through Q1 2026) yields a fair value of $24.64, supporting a revised target of $24.64.

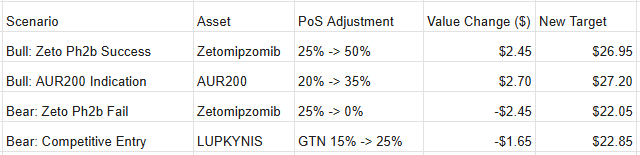

rNPV Sensitivity Analyses

LUPKYNIS Commercial Sensitivity

The following table shows how the per-share value fluctuates based on Peak Patient Penetration (out of a 32,000-patient RAM) and the Weighted Average Cost of Capital (WACC). This core segment currently accounts for ~$14.14 of the total value in our $24.64 model.

Pipeline & Clinical Sensitivity

The pipeline assets are heavily sensitive to their Probability of Success (PoS), so note how a successful Phase 2b readout for zetomipzomib (increasing PoS to 50%) or a clinical failure (0%) creates a massive swing in the fair value.

DISCLOSURE

This Due Diligence report is for informational purposes only and does not constitute financial advice or a recommendation to buy, sell, or hold any securities. The information is based on public filings and media reports and may not be exhaustive or entirely accurate. Investing in biotechnology companies, especially those in clinical stages of development, involves inherent risks, including the complete loss of capital. Clinical trial outcomes, regulatory pathways, and eventual commercial success are subject to uncertainty. Readers should conduct their own thorough due diligence and consult with a qualified financial advisor before making any investment decisions. The author may hold long positions in Aurinia Pharmaceuticals ($AUPH) and has received no compensation for this report.

A rare one I don't have I shall dive into it.