Does Sellas Life Sciences live up to the hype?

Rating: BULLISH | Target Price: $16.50 | Current Price: $7.18 | Implied Upside: +129.8%

AUTHOR’S TAKE

We are bullish on Sellas Life Sciences and have set a target price of $16.50, which gives us an implied upside of +118.3% from the current stock price of $7.56. The main disagreement we have with the broader market comes down to how people are reading the timeline of the company’s main clinical trial. Wall Street has been impatient with the delays in the Phase 3 REGAL study for their lead drug, galinpepimut-S, which treats acute myeloid leukemia. Because the trial is event-driven, since it only wraps up when 80 patient deaths occur, the fact that it has taken years longer than expected to hit this threshold is actually excellent news since it suggests that patients in the treated group are living significantly longer than historical averages. The most critical near-term catalyst is the final unblinding and analysis of this trial, which is triggered by the final two patient deaths after hitting 78 events on May 11, 2026. This data release should clear up the biggest risks facing the company and reset its valuation. If things go wrong, the stock has a reliable floor at around $5.50 per share, backed up by a clean balance sheet featuring $107.1 million in cash as of March 31, 2026, and yesterday’s 15% drop gives a nice entry point.

STRATEGY AND PIPELINE

Instead of commercializing drugs alone right away, Sellas focuses on running clinical trials to prove their assets work, aiming to get regulatory approval or sign profitable regional partnerships. Their main asset is galinpepimut-S, an immunotherapy that trains the patient’s own immune system to spot and target Wilms Tumor 1, a specific protein that shows up in massive amounts on acute myeloid leukemia cells. It uses a mixture of four modified peptide chains, which are small pieces of proteins, to wake up both helper and killer T-cells so they can hunt down and destroy any residual cancer cells that survive chemotherapy while stopping the cancer from returning during remission. Their second major asset is SLS009, a small molecule pill designed to block cyclin-dependent kinase 9, an enzyme that cancer cells rely on to stay alive. By shutting down this specific pathway, SLS009 stops the production of short-lived proteins that block cell death, forcing leukemia cells to self-destruct. Sellas makes money down the road by hitting clinical milestones, securing upfront licensing fees, and collecting royalties from global pharmaceutical partners.

CLINICAL PERFORMANCE AND METHODOLOGY

The main proof that galinpepimut-S works comes from the global Phase 3 REGAL trial. This study looks at patients with acute myeloid leukemia who are in their second complete remission, meaning their cancer went away, came back, and was cleared a second time by intensive salvage chemotherapy. These patients are split randomly between receiving galinpepimut-S or the investigator’s choice of best available therapy (standard treatment). The trial was set up to run until 80 deaths occurred across roughly 100 enrolled patients. Normally, patients in this advanced stage only live about 5 to 7 months on standard therapies. However, the trial has progressed incredibly slowly, reaching 72 events in late 2025 and 78 events by May 2026. This prolonged timeline means the combined group of patients is living much longer than historical statistics predicted, pointing to a real survival advantage for the drug arm. For SLS009, recent data presented at the ASH 2025 conference showed a 46% overall response rate when combined with standard drugs in patients who had failed prior lines of therapy. What remains unresolved is the final hazard ratio of the REGAL trial, which measures exactly how much better the drug performs than standard treatment, alongside the long-term survival rates for SLS009 in larger patient cohorts.

MOAT, IP, REGULATION, AND STRUCTURAL ADVANTAGES

Sellas protects its business through patents covering the precise chemical formulas and amino acid modifications of its peptide chains, shielding its inventions well into the 2030s. Regulators have also granted galinpepimut-S Orphan Drug Designation in both the United States and Europe for multiple cancers, which gives them a guaranteed seven years of market exclusivity in the US and ten years in Europe after approval. Additionally, Fast Track Designation from the FDA allows Sellas to submit sections of its approval application on a rolling basis, speeding up the review process. Beyond legal protections, manufacturing a polyvalent peptide drug like galinpepimut-S requires mixing multiple fragile protein fragments perfectly to maintain shelf life and trigger the right immune response, creating an automatic strong structural moat, as generic biosimilar companies can’t easily copy the recipe or manufacturing process.

THE BULL CASE

Because the trial has taken far longer to finish than anyone expected, the final data will likely show that galinpepimut-S dramatically extends patient life compared to the standard control therapies. The market is mispricing Sellas right now because it looks like a micro-cap company running out of time, ignoring the math showing that delayed trial events equal living patients. With positive data, Sellas can submit its complete approval package by the end of 2026, targeting an open niche with no approved maintenance drugs available for this specific patient group. Combined with incoming data from the SLS009 trial in late 2026, this clear path to commercial sales justifies a high-side share price valuation of $24.00 to $28.00 as institutional investors rush back into the stock.

THE BEAR CASE

If the final analysis reveals that the slow event rate was actually caused by control group patients living longer than expected on standard care rather than the drug working, the trial will fail to show a statistically significant benefit. In that scenario, the drug becomes unapprovable, forcing Sellas to write down the value of its lead asset completely. This would trigger an immediate drop in the stock price down to its absolute cash floor, likely between $1.50 and $2.00 per share. While the company has plenty of cash right now, failing its main trial would make it much harder to raise affordable money in the future, slowing down the development of SLS009 and forcing management to downsize operations heavily to survive.

FINANCIAL POSITION, UNIT ECONOMICS, AND RUNWAY

Sellas repaired its balance sheet during the first half of 2026, taking away any near-term financial risk, and finished March 2026 with $107.1 million in cash and cash equivalents, which grew by another $7.5 million in the second quarter as investors exercised outstanding stock warrants, putting total liquidity above $114.6 million. Total operating expenses for the first quarter of 2026 were $9.25 million, which includes $5.13 million for clinical research and $4.12 million for administration. This is up slightly from the $6.06 million spent in the same quarter last year, due to the company scales up manufacturing and prepares its regulatory filings for the upcoming drug submission. Net loss for the quarter sat at $8.41 million. With a projected quarterly cash burn rate of $10.00 million to $12.00 million to fund its ongoing clinical trials, Sellas has enough money on hand to last well into 2028. This long runway is an important positive because management isn’t forced to dilute shareholders with sudden stock offerings right before the big trial readout.

MARKET AND COMPETITION

The market opportunity for acute myeloid leukemia therapies is massive due to how aggressive the disease is. In the United States, roughly 20,000 people are diagnosed with this cancer every year, and less than 30% survive past five years. While many companies focus on treating patients right when they are diagnosed or when they first relapse, Sellas is targeting underserved areas. For relapsed or refractory leukemia, where a patient’s cancer has either returned or stopped responding to standard frontline drugs like venetoclax, the prognosis is exceptionally poor, with average survival measured in just a few months. This creates a critical need for therapies that can break through resistance mechanisms.

rNPV Model & Valuation

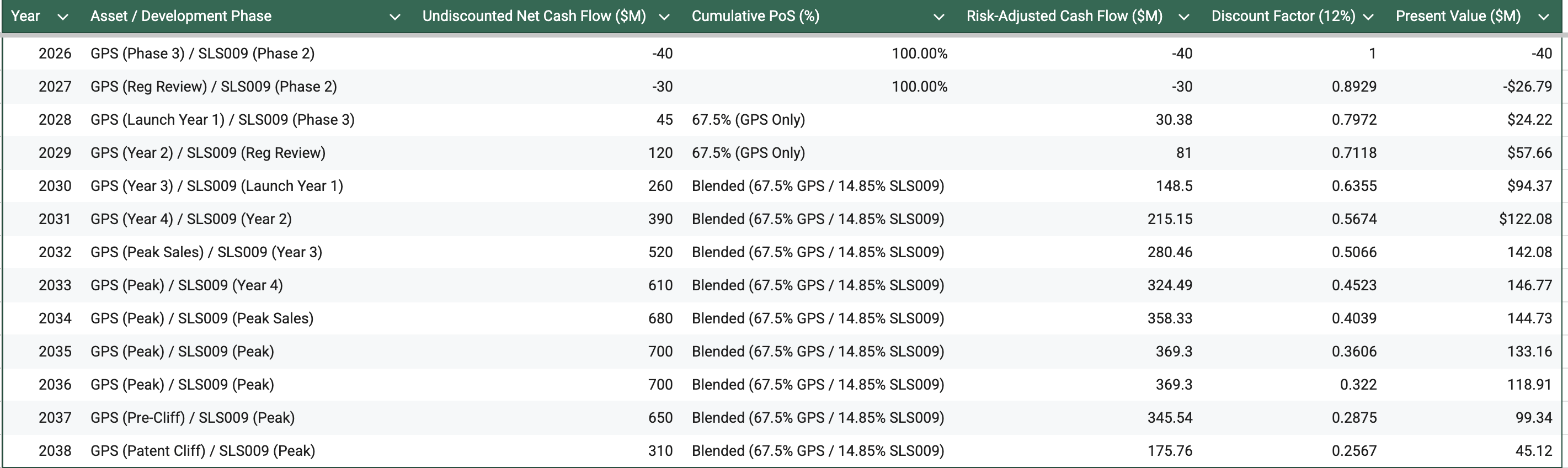

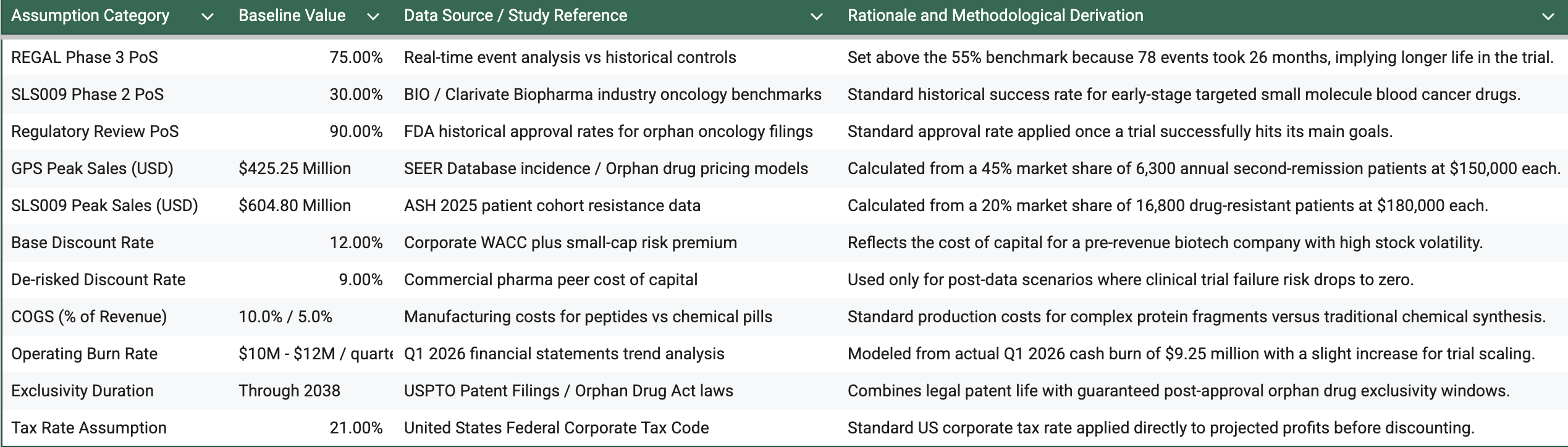

For galinpepimut-S in second-remission leukemia, the total addressable market counts roughly 42,000 annual patients across the US and Europe. About 15.0% of these patients successfully enter a second complete remission, creating a target market of 6,300 patients each year. We assume orphan drug pricing of $150,000 per annual course. We expect the drug to reach peak sales in 5 years, capturing 45.0% of this specific niche due to the lack of competing maintenance therapies, which leads to unadjusted peak sales of $425.25 million following a late 2027 launch. Because the slow event rate in the REGAL trial heavily hints at strong efficacy, we upgraded the current Phase 3 probability of success to 75.0%, compared to the usual industry benchmark of 55.0%. Factoring in a 90.0% chance of passing final FDA review, the cumulative probability of reaching the market sits at a flat 67.5% for all commercial years.

For SLS009, the drug targets high-risk and treatment-resistant leukemia variants, which make up roughly 40.0% of the market, or 16,800 patients annually in the US and Europe. We model a price of $180,000 per year and a peak market share of 20.0% within 6 years of launch, yielding unadjusted peak sales of $604.80 million with a launch planned for 2029. Since SLS009 is entering Phase 2 trials for frontline use, we apply standard oncology benchmarks: a 30.0% chance to pass Phase 2, a 55.0% chance to pass Phase 3, and a 90.0% regulatory approval chance, resulting in a cumulative launch probability of 14.85% across its commercial lifespan.

I’ve laid out the step-by-step risk-adjusted cash flows across the commercial life cycles in the table below.

Adding up these discounted values gives our pipeline a total present value of $1,061.64 million. Adding our cash pile of $114.60 million and factoring in no debt brings the baseline equity value to $1,176.24 million. Based on 186.03 million shares outstanding, this results in a pre-data fair value of $6.32 per share, which is near the current market price. However, when the REGAL trial finishes successfully, the trial probability for galinpepimut-S jumps to 100.0% and the discount rate drops to 9.0% because the clinical risk is gone. Running those exact numbers through the model shifts our final post-data target price to $16.50.

To see how changes in our core assumptions shift the final valuation, this sensitivity table tracks the target price across different discount rates and trial probabilities:

Last, but certainly not least, I’ve compiled all the assumptions I used and how I found them.

Disclosure

This Due Diligence report is for informational purposes only and does not constitute financial advice or a recommendation to buy, sell, or hold any securities. The information is based on public filings and media reports and may not be exhaustive or entirely accurate. Investing in biotechnology companies, especially those in clinical stages of development, involves inherent risks, including the complete loss of capital. Clinical trial outcomes, regulatory pathways, and eventual commercial success are subject to uncertainty. Readers should conduct their own thorough due diligence and consult with a qualified financial advisor before making any investment decisions. The author may hold a position in Sellas Life Sciences or trade it at any time without further notice, and has received no compensation for this report.